Are Credit Unions Transforming Member Experience?

The Pulse of Credit Unions

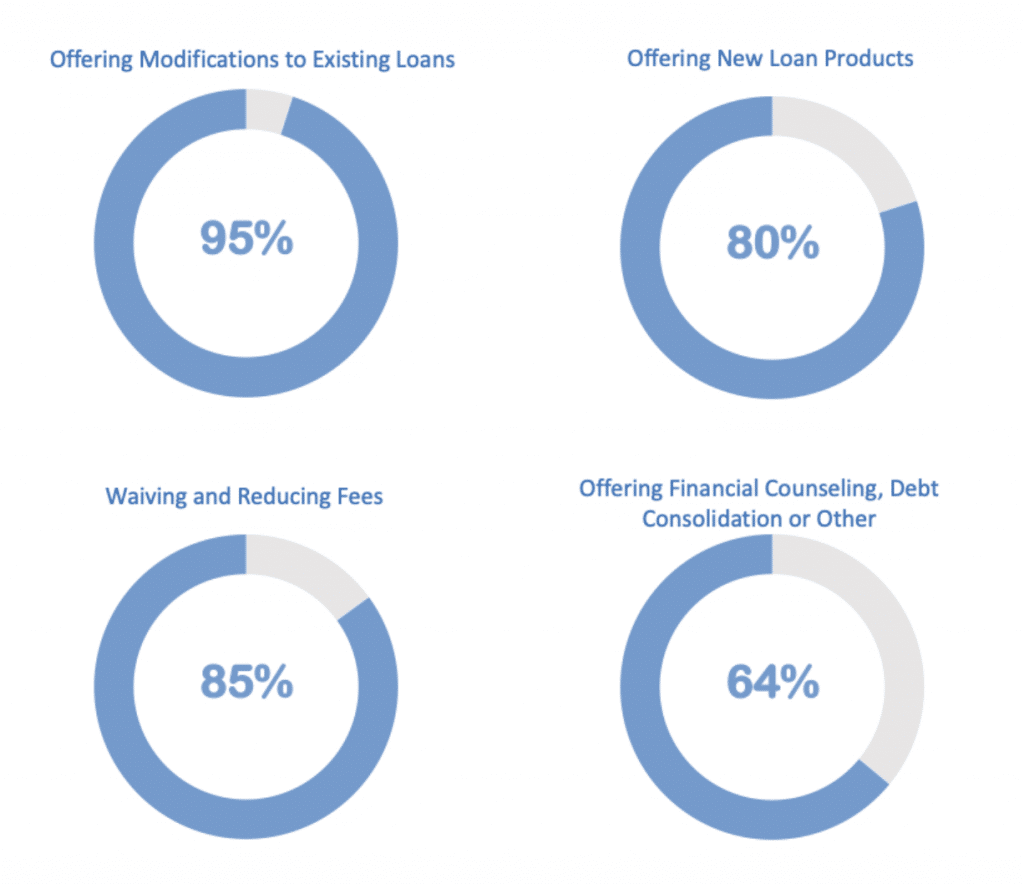

Credit Unions remain a one-stop-shop for consumers looking for options across mortgages, loans, and other credit. Also, Credit Unions that participated in the SBA’s Paycheck Protection Program (SBA PPP) have been laser-focused on supporting the smallest of small businesses, with average loan size $65,000, according to a recent CUNA/AACUL survey. The survey also highlighted credit unions have adapted well to help support their members’ financial well-being:

Credit Unions have been most flexible to member experiences and evolving to their needs. With the rise of digital technology and disruption across financial services over the last 5-10 years, CUs need to do much more to stay relevant to members. Traditional lending has been transforming through digital enablement, see “Transforming From Traditional Lending.”

Customer Satisfaction Waning

Over the past five years, Banks have significantly invested in digital transformations specific to areas of customer experience and engagement (i.e., CRM, Call Center, MarTech). Banks have capitalized on these digital investments and have established more options to engage customers across mobile and self-servicing tools. After being tied in 2018, customers gave banks a satisfaction score of 80 out of 100. Meanwhile, credit union customers rated their satisfaction at 79 out of 100, a 2.5-point dip from 2018. The staple of personalized services of smaller banks and credit unions may no longer be the differentiator for customers, especially younger demographics.

Member Generational Shifts

Credit Union members embrace tech and their demands are high. Over the years, CUs have led the charge with first to market online banking positioned for ease of use, distancing themselves from traditional banks. In many ways, being member owned and operated helped them stay close to customer needs and desires.

According to FIS, digital banking is no longer a trend. Millennials, GenX, and Baby Boomers, choose “trust” as the essential quality in selecting a banking provider, with digital self-service a close second. As the younger generations (GenZ) age, their expectations are set as “table stakes, “not differentiators.”

Having a digital focus remains a central part of the customer experience and a driver of member value, resulting in increased acquisition and retention.

Disruptors Are Looming

Banks are not the only focus. The increased pressure of Fintechs has wreaked havoc across core banking – including payments, onboarding, and self-service. As mentioned previously, traditional lending practices have become increasingly digital, making survival more difficult.

Many CUs think partnering with Fintechs solves the problem. Think again. Most, if not all, Credit Unions have a very loyal membership base. Fintechs love this as an easy entry to scale across a defined user base quickly. CU’s often mimic the approach Banks have taken here without considering the fundamentals. Traditional Banks have protected their IP and partnerships through significant investment. These investments safeguard their valuable assets from Fintech’s but still enable them as relevant partners. CU’s often don’t protect their IP, which is a major risk when working with Fintechs.

Another perceived strength is a CU’s culture (which may be a weakness). CUs tend to have a local/personalized relationship that, in many ways, is secluded from the fast-paced and ever-changing tech sector. While this does not seem like a significant risk, rapid changes/transformations hurt the Credit Union’s mission to members. In the end, buying/licensing the technology (i.e., CRM, Call Center, MarTech) provides a more organized and secure approach to engage with customers and sustain a personalized relationship, while also staying ahead of industry changes.

Security Risks

In addition to the strict field of membership, capital restrictions, and consumer protection provisions in the Federal Credit Union Act, security remains critical. Credit Union executives are concerned with the evolving regulatory environment and keeping technology current. Cybersecurity remains a real threat to board-level awareness.

The Financial Industry Regulatory Authority (FINRA) in May warned of phishing scams targeting financial professionals during the COVID crisis. These scams, combined with disaster recovery and maintaining antiqued systems across CUs, have raised significant concerns and proper use of cloud platforms. Many Credit Unions have embraced the move to cloud and should consider the technology’s functionality, security, and access controls (Identity, Authorization, Encryption, Audit).

Digital Enablement

As a boutique firm, we understand the importance of relationships and mission. Our work to enable digital and connected credit unions remains our passion. Harnessing the power to improve operational control, reduce costs, build new revenue streams, mitigate risk, and compliance is possible.

Also, member outreach during the COVID crisis is critical. Many of our clients have raised the bar on communication through optimizing Pardot and Marketing Cloud to enable notifications, alerts, and messaging across sales and servicing. From self-service to enhanced onboarding and operational support with forbearance and hardships.

Other clients have focused more on communication by optimizing their Pardot or Marketing Cloud implementations to support proactive COVID messaging and stage and status messaging to provide updates for Cases, Applications, and Forbearance or Hardship requests.

Let us help you in taking the first step to unifying solutions and drive member value:

- Create a unified view of all assets to enable the ultimate member experience

- Extend servicing through self-service and online guidance/support

- Gain full relationships across lease/loan participants and interactions

- Enhance and automate operational workflow and credit/underwriting

- Connect customers, third-parties across digital channels

- Securely maintain compliance and audit tracking requirements

Xede has tailored Credit Union solutions readily available to address changing requirements across SBA’s PPP Paycheck Protection Program, CARES Act Mortgage Forbearance, and Marketing Preference Management.

SOURCES CITED:

CUNA & State Credit Union Leagues Survey, March 2020

ACSI Finance, Insurance, and Health Care Report 2018-2019

2019 PACE Report, FIS

- The Value of Marketing Cloud Realized for Financial Services - August 14, 2020

- Are Credit Unions Transforming Member Experience? - August 10, 2020

- One Preference Center to Rule Them All: Xelerating SFMC - June 12, 2020

Connect with Xede today to start growing your business faster, smarter and stronger.